[Keywords:] online games, mobile games

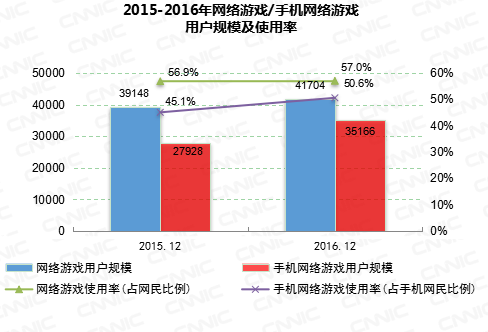

According to CNNIC’s latest 39th Statistical Report on Internet Development in China, as of December 2016, the number of online game users in China reached 417 million, accounting for 57.0% of the total netizens, an increase of 25.56 million over last year. Compared with the end of last year, the number of users of mobile online games increased significantly, reaching 352 million, an increase of 72.39 million, accounting for 50.6% of mobile Internet users. The online game industry maintained a steady development in 2016 as a whole, and the scale of mobile game users and industry revenue as the core of growth increased significantly.

Figure 2015-2016 Online Game/Mobile Online Game User Scale and Utilization Rate

Domestic PC clients have entered a trough since developing games.

The growth of domestic PC client game revenue is close to stagnation, and the income of overseas agent products is further squeezed from R&D products. After years of development, the growth space of PC-side games has gradually decreased, and the dominant market structure of large-scale manufacturers has been relatively fixed. Moreover, as the R&D focus of domestic online game manufacturers has been fully moved to the mobile side, there are few self-developed products for PC-side games listed in China in 2016. According to the public financial report data, the PC-side game revenue of most online game manufacturers has been surpassed by their mobile game revenue in 2016, and the growth rate of PC-side game revenue is much lower than that of mobile game revenue. In addition, the number of self-developed games by manufacturers is decreasing year by year, which leads to the increasing proportion of products from overseas agents in domestic PC client game revenue. The reduction of internal resources of manufacturers further reduces the possibility of game developers entering this field.

The supervision policy of mobile game industry is improving day by day.

While mobile games have become the revenue pillar of the online game industry, the government’s supervision has gradually increased, pushing the long-term extensive growth of the mobile game industry into a healthy development track. The Notice on the Management of Mobile Game Publishing Service was implemented in July 2016, which laid the foundation for improving the problems of shoddy work and piracy that have plagued the development of the industry for a long time. At the same time, it also put forward requirements for the registered capital and related qualifications of game publishers, which objectively raised the industry threshold. Although the phenomenon of piracy and infringement has been curbed, the common problems in the mobile game industry such as "mobile game brushing list" and "self-recharging" still aroused widespread concern in society in 2016. The management of chaos in such industries will be the main direction for the government to improve the rules and regulations in the next step.

The trend of oligopoly in the industry is more obvious.

With the continuous tightening of supervision, the survival pressure faced by small and medium-sized game manufacturers is gradually increasing, and the oligopoly trend of the industry is more obvious. Under the background that the domestic capital market turns cold, the online game industry’s traffic dividend disappears, the marketing cost increases, and the employment threshold rises, and the competitiveness of small manufacturers in the industry will gradually lose. According to the manufacturer’s data, by the end of 2016, the number of daily active users of Tencent’s the glory of the king had exceeded 50 million, that of Giant Network’s Ball Fight had exceeded 25 million, and that of Netease’s Yin and Yang Division had exceeded 10 million in just one month. Large-scale online game manufacturers with strong capital reserves and R&D capabilities will occupy more advantages in the future market competition, and the oligopoly trend of the industry will become more obvious. (Guo Yue, analyst of China Internet Network Information Center)

关于作者