Source: opinion leaders

Opinion Leader, Team Ren Zeping

guide reading

At the beginning of March, the "Lun Ni" incident in Qingshan appeared an epic short-selling market in the derivatives trading market, which shocked the whole world, and its ups and downs far exceeded any commercial blockbuster.The Russian-Ukrainian conflict detonated the LME nickel price on the London Metal Exchange, and Qingshan Group, as a short position of LME nickel hedging, once faced huge disk losses due to the difficulty in delivery.

The past is not like smoke, and the cycle is constantly staged. Similar shocking commercial wars triggered by international derivatives transactions have occurred many times, which also sounded the alarm for China enterprises to go to sea. The bankruptcy of Bahrain Bank,In 1995, the unauthorized trading of Nikkei stock index and interest rate futures caused huge losses, and the 233-year-old Bahrain Bank finally closed down.CAO oil crisis,In 2004, CAO Singapore sold crude oil call options, and eventually the oil price rose, resulting in a loss.The huge loss of copper in the State Reserve,In 2005, traders of the State Reserve Bureau established a large number of short copper positions in LME, and then the copper price rose sharply, causing huge losses.The huge loss of crude oil treasure,In 2020, under the influence of the epidemic, negative oil prices appeared, and crude oil products linked to international crude oil futures caused great losses.

Major trading events, such as the bankruptcy of Bahrain Bank, the huge loss of copper in China National Reserve, the aviation oil crisis, the huge loss of crude oil treasure, and the short selling of nickel, all show that derivatives are prone to long tail risk in extreme market, and participants should actively deal with the risk.

Looking at the crises caused by several major derivatives transactions in global history, we can draw five inspirations:To participate in the market, you must understand the market; Strictly divide speculative and hedging positions; Establish an effective risk management system for financial derivatives business; Deepen the construction of a high-level domestic derivatives market; Deeply understand the "black swan" in the financial market and do a good job in stress testing.

main body

1 The bankruptcy of Bahrain Bank in 1995

1.1 the whole story: opening a secret trading account, misjudging the situation, making multi-day Nikkei stock index and shorting national debt, resulting in huge losses.

Bahrain Bank opened in London in 1762, and it is one of the oldest banks in the UK, with operations in emerging markets such as Asia and Latin America. In 1994, the pre-tax profit of Bahrain Bank reached US$ 1.5 billion, and its core capital ranked 489th among 1,000 large banks in the world.On February 26th, 1995, Bahrain Bank declared bankruptcy because Nicholas, a trader of its Singapore branch, suffered huge losses and was unable to continue its business.

Without effective internal control, there are major omissions in risk management during the operation of multinational banks.Nicholas, a trader, went to work in Bahrain Bank in 1989. In 1992, he became the general manager of Singapore Futures Department, responsible for managing trading positions and hiring traders and back-office liquidators.Because there is no firewall mechanism, Allison established a secret trading account to hide trading operation losses and unapproved trading positions many times.By 1994, the accumulated losses in hidden accounts exceeded 200 million pounds. Derivatives trading positions without internal control approval are easy to quickly amplify risks under extreme market conditions.

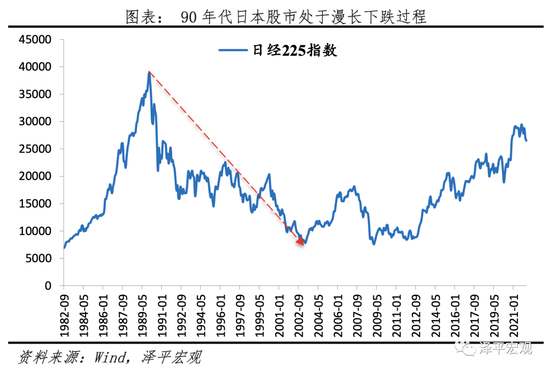

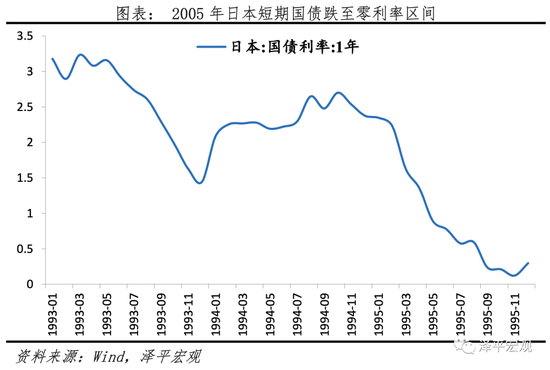

Misjudge the economic situation in Japan, speculate on the Nikkei and short Japanese bonds against the trend.In 1990s, the Japanese stock market was in a long-term downward trend due to multiple factors, such as the demographic inflection point of the long-term economy, the collapse of the real estate bubble and the trade friction between the United States and Japan. In this long-term trend, trader Nicholas misjudged the direction of the Japanese stock market.In 1995, Ellison built a trading portfolio of long-term Nikkei futures contracts and short-term Japanese interest rate bonds. But the market did not follow his expectations.First, after the Plaza Accord, the long appreciation process of the yen for many years came to an end. The exchange rate of the yen against the US dollar reached its highest in the second quarter of 1995, and the market’s pessimism about Japan’s trade exports and economic uncertainty increased sharply. Second, in January 1995, the Hanshin earthquake occurred in Japan, and the market risk aversion suddenly rose. The Japanese stock market, which rebounded briefly in 1994, returned to the downward channel again, and the yield of government bonds also fell rapidly. The interest rate of one-year government bonds fell from the high point of 2.5% in 1994 to the lowest point of 0.04% in 1995.The combined losses of long stock indexes and short treasury bonds of Bahrain Bank ended up as high as $1.4 billion.

1.2 Impact: A century-old bank went bankrupt, and the dimension of banking risk supervision was adjusted.

The century-old bank eventually went bankrupt, and global financial risks were contagious.In 1995, the 233-year-old Bahrain Bank finally closed down. After the bankruptcy,Sold to ING Group in the Netherlands at a nominal price of 1 pound.The bankruptcy of Bahrain Bank has had an impact on the international financial market. On the one hand, the global stock market has been impacted to varying degrees; on the other hand, it has disturbed the lower exchange rate of the pound; on the other hand, it has had a hidden impact on the global financial industry.

With the regulatory adjustment of Basel Accord, bank risks pay more attention to multi-dimensional considerations.The original Basel Accord put more emphasis on the consideration of bank credit risk. If only calculated by the credit risk weight, Bahrain Bank was still a bank with good capital adequacy ratio before its collapse. However, if multiple factors such as transaction risk and market risk are considered, the existence of "secret account" is a great exposure of transaction risk. In 1998, the Basel Accord was revised again, requiring that the capital adequacy ratio of banks should be combined with various risks faced by banks.Expand risk consideration to market risk and operational risk, rather than just linking capital adequacy ratio with credit risk.The New Basel Capital Accord was published in 2004 and implemented in 2006. According to the New Basel Capital Accord, banks should disclose information including capital structure, risk exposure and risk management strategy in a timely manner.

2 2004 China Aviation Oil Crisis

2.1 The whole story: from bilateral to speculation, risk control omission and unlimited jiacang.

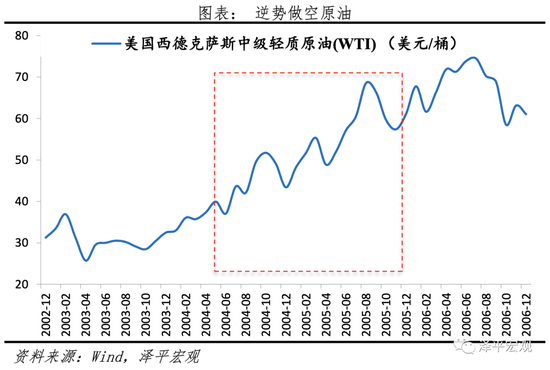

China Aviation Oil (Singapore) Co., Ltd., established in 1993, is an overseas holding company of China Aviation Oil Group Corporation and listed on the main board of Singapore Stock Exchange in 2001. As an important importer of jet fuel in China, it supplies jet fuel to airports all over China and international airports in North America and Europe. Due to the huge trade volume, CAO began to trade petroleum derivatives in 2002.

During the period of 2003-2004, CAO traded the options portfolio of short crude oil through the London oil futures market and the OTC options market, and eventually the oil price rose, resulting in a short position loss.On November 30, 2004, CAO applied to the Singapore Stock Exchange for suspension of trading.On December 1st, it was announced that the company suffered heavy losses in speculative oil derivatives trading, with a total loss of $550 million.

At first, the trading risk of CAO was not completely uncontrollable, but in the process from middleman business to speculative option trading, the position risk was gradually enlarged under the operation of extending the position and covering up the book loss with unlimited positions.

In the first stage, the risk of middleman option trading is still controllable.In 2002, CAO obtained the qualification of overseas trading and began to trade petroleum derivatives. At first, the company mostly carried out the business of middlemen, and earned commissions by trading bilateral back-to-back options, so the risk of unilateral position exposure was low.

In the second stage, speculative positions were temporarily successful.In the second quarter of 2003, CAO began to engage in speculative oil option trading. CAO began to expect the oil price to rise, and made more oil prices by making a combination of long call options and short put options. At one time, the profit exceeded one million dollars.

In the third stage, the risk of misjudging oil prices has expanded. Since October, 2003, CAO has predicted the decline of oil price, and established short positions by selling call options and buying put options. The gap between supply and demand of crude oil was widened due to the Iraq war, the international oil price rose sharply, and the loss of the company’s option speculative position continued to expand. However, at this time, the management of CAO failed to control the risk and stop the loss, and did not confirm and disclose the risk of derivatives trading in time.

In the fourth stage, the risk broke out by continuously moving positions and adding positions.From April 2004 to October 2004, CAO continuously increased its trading position. Choose to move the expired put call option by rolling, and choose the forward call contract with more expensive selling price under the background of rising oil price, so as to obtain the premium to make up for the margin gap. The final effective contract exceeded 50 million barrels, and at that time, its annual import volume was about 15 million barrels, far exceeding the range of necessary positions required for hedging. During this period, the price of WTI crude oil rose from about $30/barrel in October 2003 to over $55/barrel in October 2004.China Aviation Oil’s short speculative positions continue to be forced by rivals such as Mitsui, Goldman Sachs, Barclays Capital and Standard Bank of London, and the losses are huge.

According to the audit report issued by PWC, three major factors, such as price misjudgment, derivative valuation disclosure error and risk control duty omission, caused the company’s speculative option trading losses: First, misjudgment of oil price,From the fourth quarter of 2003, the view of oil price trend was wrong.Second, the standard of option valuation and disclosure has not been strictly enforced.The option portfolio was not valued and was not correctly disclosed in the financial statements.Third, risk management omissions,The company lacks proper and strict risk management procedures specifically for option trading, the management has not complied with the risk management policy, and the audit department and the board of directors have failed to perform the duties of derivatives risk control.

2.2 Impact: The market value was severely frustrated and forced to restructure assets.

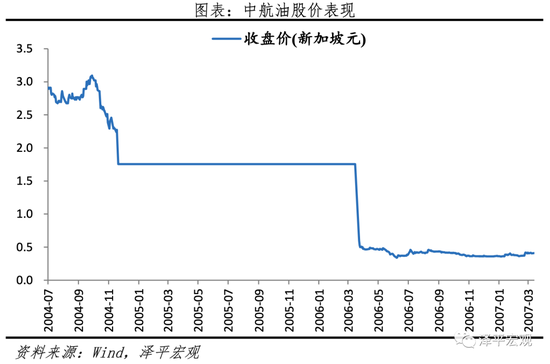

The position loss is serious, and it is insolvent.In October, 2004, due to its inability to pay a huge deposit, CAO submitted its report to the group company for the first time. Subsequently, the counterparty continuously issued a default letter to call for the deposit.The position contract of CAO has been forced and closed continuously, and the actual loss amount has been continuously expanded until it exceeds its net assets of 145 million US dollars and falls into insolvency. In December 2004, the loss reached $550 million.

The stock was suspended and its market value shrank sharply.After the incident, CAO suspended trading in November 2004 and resumed trading in March 2006 16 months later. After the resumption of trading, the stock price fell sharply for three consecutive months, and the lowest point in June 2006 reached S $0.342/share.The market value has shrunk by more than 95% compared with the peak in 2004.

The three parties participated in the asset restructuring, and BP acquired more than 20% of the restructured shares of CAO.In December, 2005, the reorganization of CAO landed. The parent company of CAO, BP and ARANDA, a subsidiary of Temasek, jointly invested 130 million US dollars, and the restructured shares of CAO, BP and ARANDA accounted for 51%, 20% and 4.65% respectively.

3 2005 State Reserve Copper Incident

3.1 The whole story: domestic copper imports increased, and traders made large short positions overseas.

The demand for copper is strong, and the dependence on domestic imports is increasing.With the acceleration of industrialization and urbanization, China’s copper consumption reached 2,736,900 tons in 2002, making it the largest copper consumer in the world. At the same time, the dependence on copper imports increased, and the net import in 2002 reached 1.104 million tons, up 40.8% year-on-year.

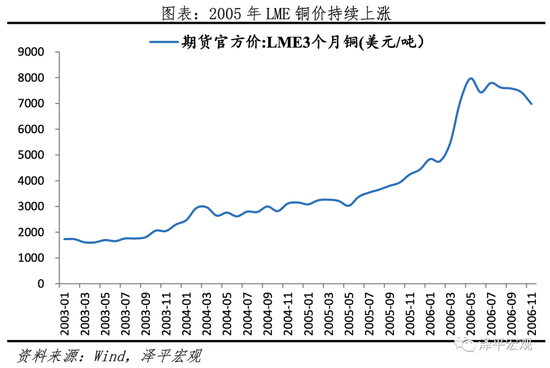

International copper prices rose rapidly, and some institutions began to be bearish.From 2003 to 2004, after the international copper price experienced a sustained rise and rapid climb, some institutions in the market predicted that the future copper price would fluctuate downward. For example, the British Commodity Research Institute predicts that there will be a surplus of global copper supply in 2005; At the LME annual meeting at the end of 2004, some international investment banks predicted that there would be room for downward adjustment of copper prices in the future.

From hedging to speculation, short positions expose risks.Liu, a "star trader" who was then director of the Import and Export Department of the State Reserve, not only engaged in hedging business, but also carried out speculative trading of futures and structured options shorting copper prices on the LME of the London Metal Exchange.Before the fourth quarter of 2005, a total of 150,000 to 200,000 tons of short positions were established near the international copper price of 3,100 US dollars/ton, and the counterparties were Smale Metal Company, Ruifu Futures, London Standard Bank, Barclays Bank, Man Group, etc. The position delivery date was December 21, 2005. Before May, 2006, the global copper price kept accelerating.The highest price of LME3 copper futures in three months is 8590 USD/ton, and the highest price of copper futures in the previous period is 85500 RMB/ton.Short positions suffered losses of about 920 million RMB.

Under the pressure of high price, the domestic copper supply is tight, and the State Reserve Bureau throws aside reserves to ease the market supply and demand.On October 30, 2005, the State Reserve Bureau announced that it would sell 30,000 to 50,000 tons of copper to the market in the near future. In November 2005, the State Reserve Bureau announced that it held 1.3 million tons of inventory, which was more than 1 million tons higher than the market expectation. From November 16th to December 7th, 2005, the State Reserve Bureau held four rounds of 20,000-ton copper reserve auctions. However, due to problems such as high auction price and spot quality, the second to fourth rounds of auctions all failed to be auctioned, and the effect of throwing copper at a lower price was not remarkable.

3.2 Impact: The trading position is losing money, the spot gap is widening, and the importance of building the local derivatives market is increasing.

Trading position losses, the spot gap widened.At that time, while facing the loss of copper trading position, the State Reserve still needed to import a large amount of overseas copper to provide spot for the market and stabilize the imbalance between supply and demand in the domestic market. As a big copper consumer and importer, China is a "natural bull" in the futures market. In the face of the rapid price increase trend, short selling is chosen, and the contract will face the risk of spot delivery when it expires. However, if some long positions are selected for hedging in the futures market, even if the subsequent copper price falls, the spot can be imported at a lower price, and the low-cost profit from spot purchase will also dispel some future positions risks.

Facing the uncontrollable risk of overseas trading, the importance of building local futures option derivatives market has been significantly enhanced.In recent years, copper options and international copper have been listed one after another, and the influence of global market prices has increased. The previous issue was listed in 2018.Copper optionIt enriches the scope of optional targets for risk management of entity enterprises, improves the market system of commodity derivatives, and further meets the level of personalized and refined risk management of enterprises. Renminbi-denominatedInternational copper futuresThe contract was officially listed and traded in the last energy center in November 2020, and the domestic copper futures officially formed a "double contract" pattern. International copper futures reflect the supply and demand of the international market and enhance the price influence of China in the global copper market.

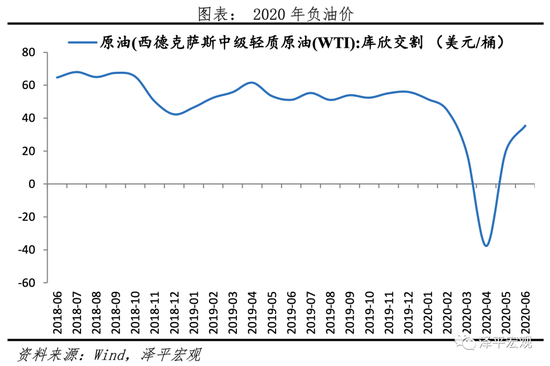

4 2020 Crude Oil Treasure Event

4.1 the whole story: oil prices turned negative under the epidemic situation, and long positions were lost.

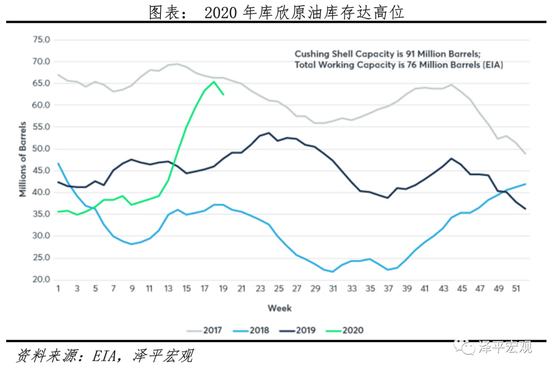

The epidemic affected the imbalance between supply and demand, and global oil prices plummeted rapidly.In the first quarter of 2020, the epidemic caused the global production and operation activities to stagnate, the capacity utilization rate of overseas refineries fell sharply, and crude oil inventories reached a new high. Crude oil stocks in Cushing, Oklahoma, where US crude oil futures are delivered, continue to increase. According to EIA data, the inventory in Cushing once reached 65 million barrels, while the actual available storage capacity in Cushing was 76 million barrels, and the inventory once exceeded 85% of the storage capacity. The problem of "difficulty in storing oil" affected the long maturity of WTI crude oil futures contract in May, and it was difficult to deliver the spot. At one time, there was a "empty force" market.

The exchange temporarily revised the rules, and WTI crude oil futures contracts once had negative oil prices.On April 3, 2020, CME Exchange issued a notice to modify the code of IT system, allowing negative price declaration and transaction for the first time. Further communication with clearing companies and customers on April 8 does not rule out the possibility of negative oil prices. April 20th (the early morning of April 21st, Beijing time) was the last trading day of May 2000 contract. As the position of delivery contract decreased, the price fluctuation was easily amplified by the influence of large funds. At one time, the WTI oil price of CME Exchange was as low as -40 USD/barrel, and the settlement price reached -37.63 USD/barrel.

Crude oil products are linked to contracts in recent months, and the time difference between transaction settlement magnifies the loss of moving positions.The "Crude Oil Treasure" product was launched by China Bank in January 2018, providing domestic individual customers with trading services linked to overseas crude oil futures. Among them, American crude oil varieties are linked to the first contract of Texas light crude oil WTI futures of CME of Chicago Mercantile Exchange. Individual customers’ participation in crude oil investment is a leveraged transaction, which requires 100% margin.

In terms of setting trading rules, 1) products are agreed to be linked to futures contracts, and rolling contracts need to be moved or offset when the contracts expire.Among them, netting refers to only closing all the current contracts held and settling the trading profit and loss; Moving positions refers to closing all the current contracts held and opening the next contracts at the same time.2) The time difference between the transaction set by the product and the actual settlement exists objectively.According to Bank of China, the last trading time for domestic investors of crude oil products for the May 20 contract is 22: 00 pm Beijing time on April 20, and the settlement price is calculated by using the average WTI trading price from 2: 28 am to 2: 30 am Beijing time on April 21.Therefore, long-term customers who didn’t take the initiative to offset or move positions in rolling contracts before 22 o’clock on the evening of the 20th can only settle with negative oil prices in the early morning of the 21st, facing the risk of wearing positions and "owing" bank deposits.

4.2 Impact: Individual customers lose money, and banks face the risk of punishment and compensation.

Individual investment customers are exposed to risks, such as short positions and "back-owed" deposits.Some customers choose to solve the dispute of crude oil warehouse penetration through civil litigation, and the final judicial decision is that "China Bank will bear all the warehouse penetration losses and 20% of the principal losses, return the deducted margin balance in the original account, and pay the corresponding capital occupation fee".

As the issuer of structured product design, banks face the risk of punishment and compensation.In December, 2020, China Banking and Insurance Regulatory Commission conducted an investigation on the risk incident of "Crude Oil Treasure" products of China Bank according to law, and made a decision on administrative punishment for the illegal acts involved, and took corresponding regulatory measures. First, product management is not standardized, including unclear contract terms related to margin, independent post-evaluation of products, and failure to carry out stress testing related work on products; Second, risk management is not prudent, including defects in setting market risk limits, irregular adjustment and over-limit operation of market risk limits, and defects in trading system functions that are not rectified in time as required; Third, the internal control management is not perfect, including unreasonable performance appraisal and incentive mechanism, insufficient performance protection of consumers’ rights and interests, and the internal control compliance inspection of the whole bank did not cover the sales management of private products by the Global Marketing Department. Fourth, the sales management is not in compliance, including the age of individual customers does not meet the access requirements, some promotional sales texts are exaggerated or one-sided, and products are sold by giving away in kind. China Bank and its branches were fined a total of 50.5 million yuan.

5 2022 Qingshan Lun Nickel Incident

5.1 The whole story: the conflict between Russia and Ukraine affected spot delivery, and the extreme market amplified the losses of short hedging trading end.

In March, 2022, the conflict between Russia and Ukraine aggravated the rise of nickel price. As a short seller of LME nickel, Qingshan Group faced a certain amount of disk loss in its hedging position, and needed to close the position one after another, pay the deposit, or use the spot standard specified by LME for delivery.

Qingshan has high-quality nickel spot production capacity, and the futures short hedging position is reasonable.Qingshan Group is engaged in nickel mining, ferronickel stainless steel smelting, continuous casting billet production and plate, rod and wire processing. The raw materials and intermediate products produced are also used in the field of new energy vehicle batteries. Qingshan Group owns high-quality laterite nickel ore in North Maluku, Indonesia, which is oriented to ferronickel industry and ternary battery industry of new energy vehicles. In December 2021, the first production line of high nickel matte in Qingshan Park, Indonesia was officially put into production. According to the data of official website, Qingshan has more than 10 million tons of crude stainless steel production capacity and 300,000 tons of nickel equivalent ferronickel production capacity, accounting for about 20% of the global stainless steel supply. In view of the fact that Qingshan Group holds a large number of high-quality nickel ore, ferronickel, high-grade nickel matte spot and capacity resources, it has a large nickel short hedging position in LME in order to lock in the future price and profit.

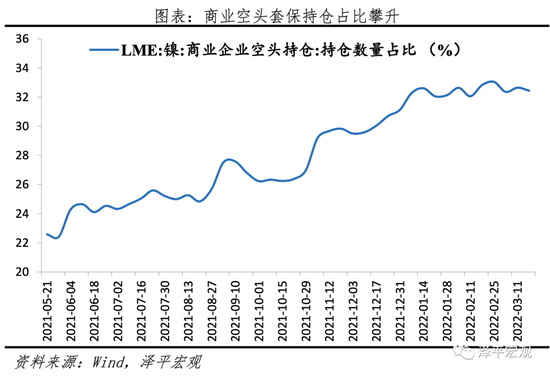

The supply and demand of nickel are tightly balanced, and the extreme market enlarges the loss of commercial short-selling trading end.In recent years, the development of global new energy vehicle industry has supported the growth of global nickel demand, but factors such as unstable supply exist objectively under the epidemic situation, and the price of nickel has risen rapidly from the relative low of $11,000/ton in 2020. At the same time, the proportion of short speculative positions has narrowed and commercial hedging positions have increased. According to LME disclosure data, as of March 2021, the proportion of commercial positions in short positions in nickel futures market rose to more than 32%. Under extreme market conditions, short positions of commercial enterprises face certain losses in hedging transactions, and it is still necessary to observe the spot production and operation costs of enterprises. If the production cost is much lower than the price level of hedging short, the profit of spot delivery can offset the loss of some hedging positions.

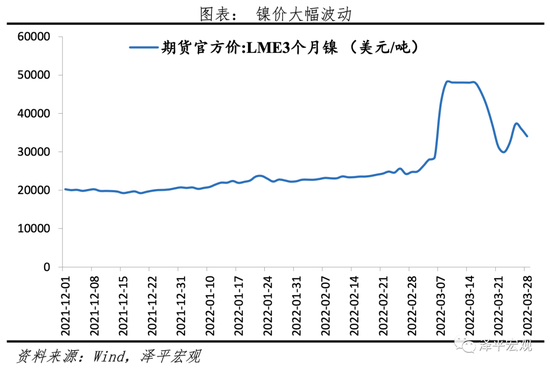

The conflict between Russia and Ukraine affects the export of spot nickel plates, and the standard delivery products of LME nickel futures are insufficient.Russia is a big country in nickel mine, and its proven reserves, output and export account for 7.86%, 9.3% and 7% respectively in the world. After the escalation of the Russian-Ukrainian conflict, the market’s concerns about the supply risk of Russian nickel mines escalated rapidly. On March 7, 2022, LME nickel rose sharply from $29,000/ton to a maximum of $55,000/ton. On March 8, the price of LME nickel continued to rise, reaching a maximum of more than $100,000/ton. According to LME standard, the nickel content of the standard delivery products corresponding to its nickel futures is not less than 99.8%, mainly electrolytic nickel, nickel plates and nickel beans, and Russian nickel plates are the main nickel delivery products of LME. However, the nickel content of mainstream nickel products in other markets, such as ferronickel and high matte nickel, is about 15%-40% and 50%-75% respectively, which does not meet the LME nickel futures delivery standard, so Qingshan may not be able to deliver directly with its own resources.

5.2 All parties should respond: LME stops trading urgently, sets up the ups and downs, and Qingshan and the syndicate reach a silence agreement.

LME Exchange should cancel extreme market transactions and set up ups and downs.After the crisis, LME Exchange cancelled the trading on the 8th and settled the two parties at the closing price of about USD 50,000/ton on the 7th, which also reduced the biggest loss of Qingshan Group to a certain extent. After that, the nickel was suspended for several days until the trading resumed on the 16th. After the recovery, the previous ups and downs system was adopted, and the nickel was adjusted back to around $30,000/ton.

A silent agreement was reached, and the overall loss was still controllable.On March 15, 2022, Qingshan Group announced that it had reached a silent agreement with a syndicate composed of creditors of futures banks. During the silent period, Qingshan and Syndicate will provide standby and guaranteed liquidity credit for nickel position margin and settlement requirements. The participating futures banks will not close positions in Castle Peak, or ask for additional margin for existing positions. Subsequent Qingshan Group will reduce its existing positions in a reasonable and orderly manner with the elimination of abnormal market conditions.

6 Enlightenment from all previous major derivatives risk events

Times have changed, but the past is not like smoke, and the cycle is constantly staged. From the collapse of Bahrain Bank in the past 100 years to the recent Qingshan Lun Nickel incident, similar events that triggered the long tail risk by derivatives trading have occurred many times in history. Looking at several major derivatives trading risk events in history, we can draw the following five inspirations:

1) To participate in the market, you must know the market.In the nickel incident, LME had clear requirements for the delivery specifications of nickel futures. The conflict between Russia and Ukraine made it impossible for Russian nickel to meet its spot standards to be delivered smoothly, and LME did not explicitly limit the intraday price rise and fall of nickel at first, which eventually led to a sharp rise in prices in a short time and the participants were "forced to empty". In the crude oil treasure incident, CME urgently revised the terms to allow negative oil prices to appear, which laid a certain hidden danger for multi-party traders facing the expiration of recent contracts.It is of great significance for extreme risk control to understand the market rules and pay attention to the differences between different exchanges in terms of trading participation principles, price fluctuation range and maturity delivery system design.

2) Strictly divide speculative and hedging positions.In the CAO incident, we saw that it gradually confused hedging positions with speculative positions. From bilateral transactions to unilateral speculation, with the omission of internal control and risk control and unlimited jiacang, the risks were relatively controllable and gradually enlarged. In the event of the State Reserve Copper, China, as a big copper consumer and importer, was required to cover the risk of future price increase by its "natural long position" in the market. However, in the face of the rapid price increase, it was easy to face the double dilemma of losing trading position and widening spot gap. In 2020, the State-owned Assets Supervision and Administration Commission (SASAC) issued the Notice on Strengthening the Management of Financial Derivative Business, requiring the financial derivative business of central enterprise groups to define the "spot exposure" and realize the "integration of period and present" management.Hedging should start from the spot, aiming at reducing the spot risk exposure, and match the spot variety, scale, direction and term. Strictly divide speculative and hedging positions, reduce excessive long and short positions under the lack of spot support, reduce risk exposure, and enhance the ability to defend against market risks.

3) Establish an effective financial derivative business risk management system.The opening of trading secret accounts by traders of Bahrain Bank and the failure of CAO to report the position loss to the group company in time all reflect that the internal control review of the risk of derivative positions by participating enterprises needs to be strengthened. Establish an effective risk management system for financial derivative business,First, improve the internal control mechanism,Define risk management requirements, approval procedures, stop loss limit, emergency treatment, supervision and inspection and accountability.The second is to strengthen risk early warning,Use quantitative and qualitative methods to identify market risk, credit risk, operational risk and liquidity risk in time, and clarify the disposal process of various types of risks.Third, improve the information system,Accurately record and transmit transaction information.Establish an effective risk management system for financial derivative business, and realize risk control in all aspects of pre-prevention, in-process monitoring and post-treatment.

4) Deepen the construction of a high-level domestic derivatives market.From the temporary modification of CME rules to allow negative prices, to the frequent trading of LME nickel after the resumption of trading, it is clear to the market that we can not blindly trust the international market. Deepening the construction of high-level domestic derivatives market and steadily promoting the internationalization of domestic futures options market are of great significance to further expand China’s financial opening up.

First, we will continue to increase the variety of tradable futures options, open wider to the outside world, promote green development and the listing of internationally linked varieties, increase market capacity and enrich liquidity.In 2021, 94 kinds of futures options were listed in China, covering agricultural products, ferrous metals, precious metals, energy, chemicals, finance and other fields, with a cumulative turnover of 7.5 billion lots and a turnover of 581 trillion, up by over 22% and 32% year-on-year, ranking first in commodity derivatives trading in the world.

The second is to enrich diversified delivery and reduce the hedging risk of enterprises.In this nickel crisis, due to the standard difference between LME nickel delivery products and the actual nickel products of hedging enterprises, the risk of "short selling" was amplified and the price fluctuation range was expanded. Therefore, for the construction of derivatives market, we should actively expand the scope of standard products of the same category deliverable targets, close to the actual situation of the industry, and convert them according to the scale of form, grade and content. Linking the diversification of spot supply and demand in the market with the standardization of derivative contracts, promoting the circulation of warehouse receipts between the off-market and the off-market markets, ensuring the close connection between spot supply and demand and the futures market, and reducing the risk of forcing more and more, is of positive significance to promoting the smooth operation of prices and enhancing the global pricing ability of the domestic derivative market.

5) Deeply understand the "black swan" in the financial market and do a good job in stress testing.In 2020, there was a negative oil price in the world. In 2022, the price of nickel catalyzed by the Russian-Ukrainian conflict rushed to $100,000. In recent years, the uncertainty of the international economic, trade and geographical situation has intensified, and panic easily leads to extreme market trends in financial markets. Under this pattern, participants in financial products, especially derivatives, need to have a penetrating understanding of product design and do a stress test on the long tail risk pushed up by the "Black Swan" incident.